As generative AI matures across underwriting, claims, and policy servicing, the insurers gaining the most ground share a common trait. They have stopped asking whether the technology can be trusted and started building the structures that make it trustworthy.

That shift in framing matters. Generative AI is not simply a faster way to do what rule engines already do. It can interpret complex, unstructured information, including claim narratives, medical records, and broker submissions, in ways that rigid, deterministic systems cannot. That capability is genuinely valuable. But capturing it requires understanding how the technology actually works and governing it accordingly.

The executives who get the most from generative AI are not those who demand it behave like traditional software. They are the ones who invest early in governance, workflow design, and human oversight, and then scale with confidence.

The Critical Distinction Between Generative AI and Deterministic Systems

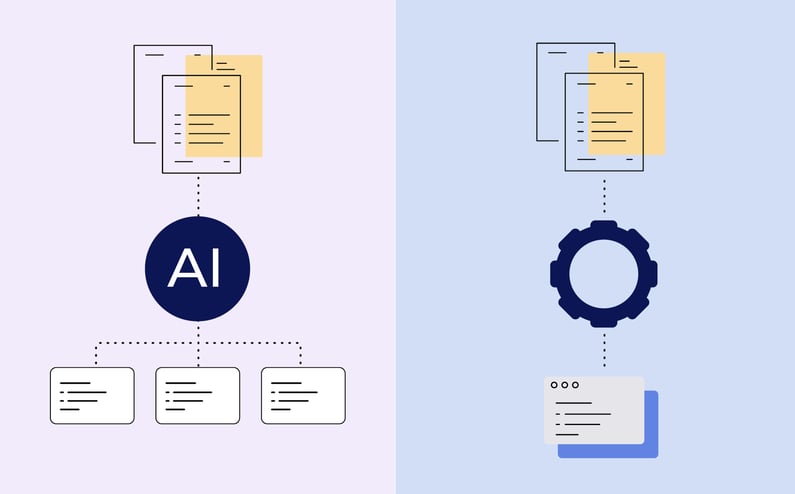

Traditional rule-based systems are deterministic: the same input always produces the same output. Generative AI for insurance operates differently.

These systems are probabilistic. They evaluate patterns learned from large volumes of data and generate responses based on likelihood rather than fixed rules. That is not a limitation to be managed around – it is the architectural reason generative AI can handle the variation, ambiguity, and unstructured complexity that rule engines cannot touch. The same input can reasonably produce different outputs, and in insurance, that flexibility is where the real value lies.

Deterministic Expectations Can Create Risk

Misunderstanding how generative AI works can lead to poor implementation decisions and two specific failure modes.

-

Overreliance. If teams assume outputs are fixed and infallible, they may bypass appropriate review or fail to monitor performance over time.

-

Premature technology dismissal. Some organizations dismiss generative AI because outputs are not identical every time, even when results are accurate and useful within acceptable tolerances.

Insurance operations already manage similar reality. Human reviewers do not produce identical summaries or classifications every time, yet organizations maintain quality through standards, training, and oversight. Generative AI should be managed with the same discipline.

Generative AI and Regulatory Compliance in Insurance

A fair criticism of generative AI in regulated industries is that variable outputs make it difficult to guarantee regulator-approved wording in every customer interaction. If a system can phrase the same disclosure two different ways, how can an insurer be certain every customer received compliant language?

This is a legitimate concern, and it points to a workflow design problem more than a technology limitation. The same probabilistic capability that creates variability in customer-facing language is what allows generative AI to interpret a complex medical record, triage an ambiguous legal demand, or synthesize a multi-document claim file — tasks that deterministic systems simply cannot perform.

Generative AI is not well suited to be the sole delivery mechanism for mandatory regulatory language. That content should be handled through deterministic controls, templated outputs, or locked disclosure language sitting outside the generative layer. Where generative AI and AI agents add value in regulated workflows is in the surrounding tasks: summarizing unstructured documents, triaging incoming communications, drafting internal notes, or synthesizing claims narratives for human review.

On auditability, well-designed generative AI implementations support logging and traceability. Inputs, outputs, confidence scores, and human review decisions can be captured, creating an auditable record of how a decision was reached even when the language varies. This is not the same as reproducing identical outputs, but it satisfies the regulatory requirement that organizations demonstrate what happened, why, and who was accountable.

Hallucinations are a real risk and should be treated as such. They are best mitigated through human-in-the-loop review, confidence thresholds that route uncertain outputs for escalation, and validation rules that flag responses falling outside acceptable parameters. Organizations that deploy generative AI without these controls are taking on unnecessary risk. Those that build governance in from the start are not.

How Insurers Can Govern Generative AI Effectively

Nondeterministic does not mean uncontrolled. Insurers can – and should – apply strong levers of governance and accountability across the lifecycle of AI-enabled workflows.

-

AI should operate within clearly defined workflow boundaries, with confidence thresholds and exception handling procedures that route higher-risk cases to human review.

-

Well-designed prompts, validation rules, and formatting standards improve consistency while preserving the flexibility that makes generative AI valuable.

-

Human-in-the-loop review plays a critical role. Reviewers provide judgment, override capability, and continuous feedback to improve performance over time.

During early implementations, higher levels of review help to ensure accuracy, refine configurations, and build organizational trust. As performance stabilizes, review can be expanded to target exceptions, low confidence outputs, or higher risk decisions, allowing insurers to scale efficiently while maintaining oversight.

Governance structures should also account for model updates and versioning. When a model is retrained or fine-tuned, its outputs can shift in ways that go beyond normal probabilistic variation. Human reviewers are often the first to detect these shifts, and a well-trained reviewer who flags unexpected output patterns provides an early warning system that automated monitoring alone may miss. Change management, human oversight, and ongoing performance measurement together form the foundation of any mature AI program.

These controls allow insurers to manage generative AI with the same rigor applied to underwriting guidelines, claims authorities, and operational standards.

Accountability does not shift to the model or the vendor. It remains with the insurer, just as it does with any operational capability.

Governance is a foundational capability, not a compliance exercise. Strong governance should be established before AI is scaled, not after problems emerge. Effective organizations formalize cross-functional oversight that includes operations, risk, compliance, and technology leaders. They define acceptable use, validation standards, escalation paths, and performance thresholds before systems are deployed broadly.

Training is equally important. Employees must understand what AI is designed to do, where human judgment is required, and how to respond when outputs appear incorrect or incomplete. Clear roles, documented workflows, and defined review points ensure accountability is maintained in daily operations.

Organizations that treat governance as a foundational capability are better positioned to scale AI safely and to move faster than competitors who are still debating whether the technology can be trusted.

Generative AI does not reward the organizations that move fastest. It rewards the ones that build well. The technology's value is real, but it is unlocked by the quality of the governance around it, not by the sophistication of the model itself. What matters most to any insurance workflow is accuracy, repeatability, and completeness, not identical phrasing.

The organizations best positioned to benefit are those that stop asking whether generative AI is safe enough to use and start asking how to deploy it responsibly.

Insurers that invest early in clear workflows, human oversight, defined standards, and honest performance measurement are not slowing themselves down. They are building the foundation that makes confident, sustained scaling possible. Generative AI is not a replacement for judgment or compliance discipline. It is a force multiplier for insurers that already have those things in place.

That discipline is not the cost of adopting generative AI. It is the differentiator.